Post-Election: - The UK’s economic challenges....

Why it's still.. "the economy, stupid".....

The UK General Election 2015 is over. The economy won the day: despite the disappointing UK growth figures half way through the campaign, the perceived threat of handing over the economic reigns to Labour, with or without the Scottish Nationalist Party in a coalition, was a strong force underpinning the Conservative’s victory. There may well be a post-election feel-good factor: the immediate aftermath of the election saw Sterling and the FTSE 100 rise and while the FTSE has fallen back, this is because of broader issues in Bond markets. Sterling has continued to rise against the US Dollar.

But before the new administration gets too comfortable, it is worth bearing in mind that its real challenges have only just begun. Quite apart from the well-documented tightening of the UK purse post-election, quite apart from the dangers of ever-rising house prices and quite apart from the equally well-documented productivity shortfall, the UK government faces three distinct problems as it starts its next five years in office...

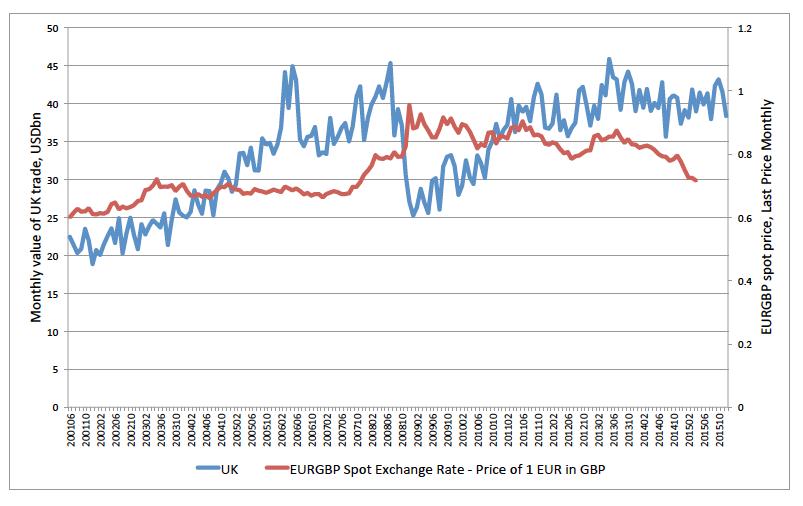

The first is the prospect for export-led growth which dominated the real growth debate in the previous administration. As the value of Sterling strengthens, this objective becomes more difficult. Of course, on one level, a strong pound helps the British consumer: imports and holidays are cheaper, and it fuels demand-led economic growth. However, although the correlation is not strong, at just 50% against the Euro and 27% against the US dollar, a stronger value of Sterling will have a negative impact on UK exporters in highly price-sensitive markets (Figure 1).

Figure 1: Value of UK exports vs EURGBP spot price, last price monthly, June 2001-Dec 2015 (forecast)

Source: DeltaMetrics 2015, Bloomberg

The second is the UK’s trading relationship with Europe given the promised Referendum on European membership scheduled for 2017. Trade with Europe accounts for 43% of the UK’s goods trade and while this grew relatively strongly before and after the financial crisis, it has fallen back considerably since 2012 (Figure 2). Some of this is because of weak demand in Europe and a reorientation towards growth markets in Asia, particularly China. However, after 2019 we see some slowdown in the UK’s trade with Europe which, although potentially picking up into the next decade, is unlikely to regain the momentum of the pre-crisis era.

.jpg)

Figure 2: Change in UK trade with Europe, %, (2002-2030 – forecast)

Source: DeltaMetrics 2015

And third, there is the issue of Scotland following the SNP’s landslide victory. The route towards the break-up of the United Kingdom may have become inevitable given the overwhelming scale of the swing towards the nationalist agenda in Scotland. This will have economic as well as political consequences. For example, and at first sight, the exit of Scotland from the United Kingdom would harm the rest of the UK far more than it would Scotland. Taking oil exports from the UK’s trade balance would add to a burgeoning energy trade deficit by around £1.6bn by the end of 2016. The trade deficit (net X) is already a drag on the UK’s GDP growth and adding to it would cramp what is still a fragile recovery.

However the big consequence is actually in the breakdown of what is an effective currency and customs union. According to UK government calculations, some 80% of Scotland’s GDP is dependent on free trade with the rest of the UK. This includes oil, of course, but equally financial services and whisky – two of Scotland’s other leading export sectors. In other words, a large proportion of Scotland’s economic performance relies on the performance of England, Wales and Northern Ireland as well. The UK is arguably the world’s oldest and most successful currency union and Free Trade Area. The Bank of England is, already, the lender of last resort ready to support Scottish banks and the Scottish deficit with UK taxpayers’ money while Scotland currently has substantial fiscal and political autonomy. Negotiating the infamous Barnett Formula may be a breeze compared to the likely challenges of restructuring Scottish debt from outside of a full UK customs union.

And take this as an example: were there a second referendum with a vote to leave the UK, then on Friday 19th September, policy makers in Scotland and the rest of the UK have to work out the terms under which Scotland can join a currency union as an independent nation. Effectively the Union suddenly faces the same challenges as the Eurozone: how to integrate a deficit nation into a structure where a transfer union (i.e. cross-border tax transfers) would be necessary to correct the internal imbalances between members of the union. A transfer union would legitimately be frowned upon by UK taxpayers if Scotland had its own tax-raising powers. But it would ensure that the lender of last resort (i.e. the Bank of England) does not have to loosen fiscal policy through greater Quantitative Easing (QE) in order to underwrite the Scottish deficit which currently stands at £12bn and which will grow if, under Scottish independence, the new administration undertakes to deliver on its expansionary promises.

All of this uncertainty will have consequences for markets. The weakness of the correlation between trade and the value of Sterling highlights this: Sterling is used as a speculative currency rather than a trade currency but there are consequences for exporters nevertheless. Further, there are already uncertainties brewing around the possibility of a Brexit from Europe; the challenges of productivity and long term growth remain as persistent now as they have ever been; the strong value of Sterling does not currently seem to be impeding trade because of the weak correlation between trade and the value of Sterling, so export-led growth is more likely to be driven by longer term competitiveness and productivity growth. The risk of a breakup of the UK before last September’s Referendum has now become a reality of the next Parliament, whose responsibility will be to transition towards full fiscal autonomy for Scotland without risking the currency union that has held for so long.

The economic honeymoon may well be very short if these considerations gather momentum.

(1).png)

Dr. Rebecca Harding, Trade View, 12th May 2015